The Ultimate Guide To Mortgage Investment Corporation

Table of ContentsThe Definitive Guide to Mortgage Investment CorporationMortgage Investment Corporation for BeginnersThe 25-Second Trick For Mortgage Investment CorporationFacts About Mortgage Investment Corporation RevealedThe 9-Minute Rule for Mortgage Investment CorporationThe Facts About Mortgage Investment Corporation Uncovered

After the lender sells the finance to a home loan capitalist, the lending institution can use the funds it receives to make even more financings. Besides providing the funds for lenders to develop more financings, capitalists are essential due to the fact that they set guidelines that contribute in what sorts of fundings you can obtain.As property owners pay off their home loans, the settlements are accumulated and distributed to the personal capitalists who purchased the mortgage-backed securities. Because the financiers aren't safeguarded, conforming lendings have stricter standards for establishing whether a debtor qualifies or not.

Department of Veterans Matters sets guidelines for VA finances. The United State Division of Farming (USDA) establishes standards for USDA fundings. The Government National Mortgage Association, or Ginnie Mae, manages federal government home loan programs and guarantees government-backed finances, shielding exclusive financiers in case borrowers default on their finances. Jumbo loans are home mortgages that surpass conforming loan limits. Due to the fact that there is even more danger with a bigger home loan amount, jumbo fundings often tend to have more stringent borrower qualification demands. Investors likewise manage them in a different way. Conventional jumbo car loans are normally as well big to be backed by Fannie Mae or Freddie Mac. Rather, they're sold directly from lending institutions to personal investors, without including a government-sponsored business.

These companies will certainly package the lendings and market them to personal capitalists on the secondary market. After you shut the lending, your lender might sell your finance to a financier, yet this generally does not change anything for you. You would still make settlements to the lender, or to the home mortgage servicer that manages your mortgage settlements.

The Ultimate Guide To Mortgage Investment Corporation

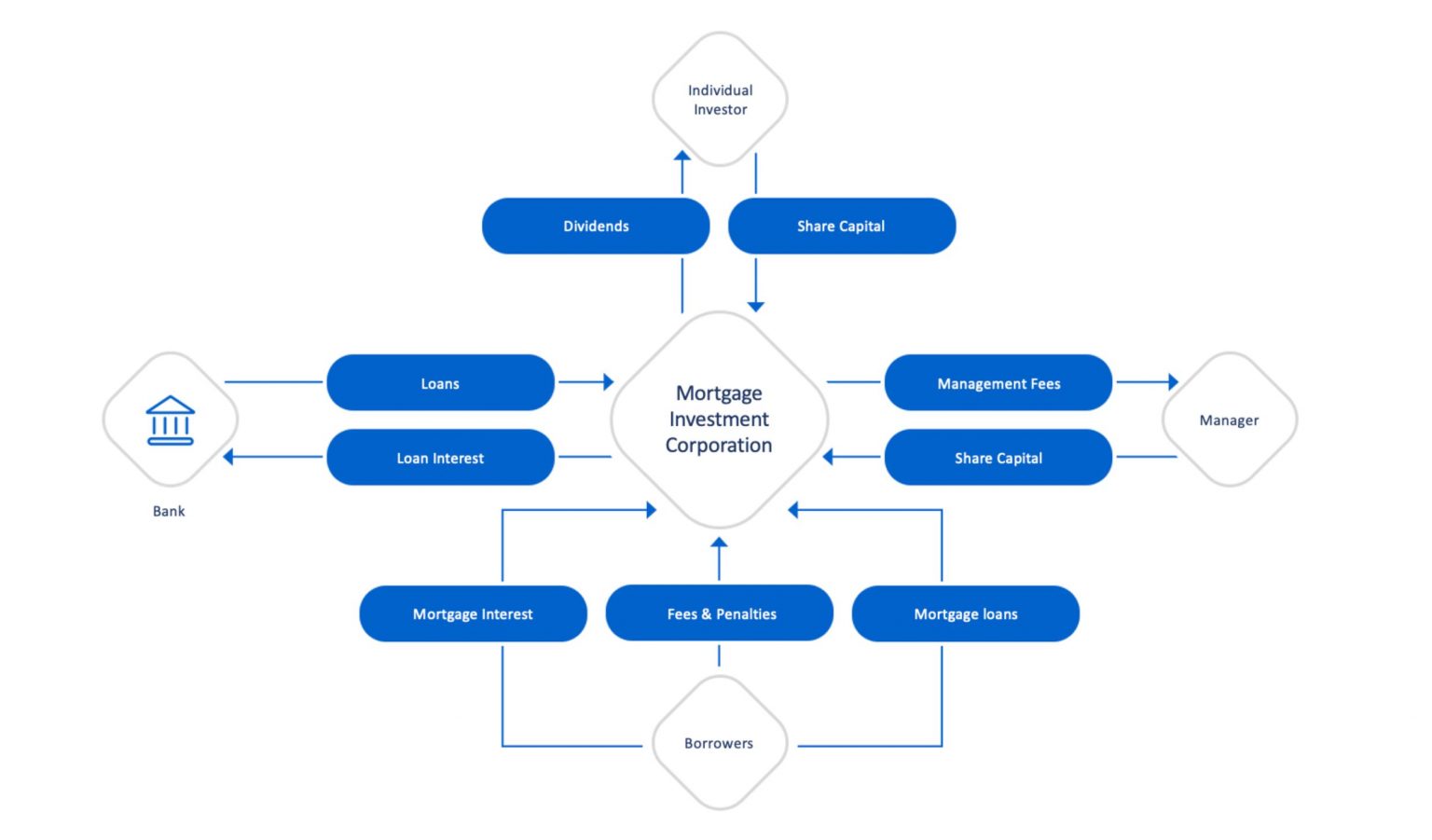

Exactly How MICs Resource and Adjudicate Loans and What Takes place When There Is a Default Home loan Investment Corporations offer financiers with direct exposure to the property market through a swimming pool of meticulously picked mortgages. A MIC is responsible for all aspects of the mortgage spending process, from origination to adjudication, consisting of daily monitoring.

CMI MIC Funds' strenuous credentials procedure enables us to take care of home mortgage top quality at the very beginning of the investment procedure, minimizing the possibility for repayment concerns within the finance profile over the term of each home loan. Still, returned and late payments can not be proactively taken care of 100 percent of the moment.

We buy mortgage markets throughout the nation, enabling us to lend throughout Canada. For more information regarding our investment procedure, contact us today. Call us by filling in the type listed below to find out more about our MIC funds.

Mortgage Investment Corporation for Beginners

At Amur Resources, we intend to provide a genuinely varied strategy to different financial investments that take full advantage of return and resources conservation. By supplying an array of traditional, revenue, and high-yield funds, we cater to a variety of investing objectives and choices that match the demands of every specific capitalist. By acquiring and holding shares in the MIC, investors obtain a symmetrical possession rate of interest in the business and get income through dividend payouts.

Additionally, 100% of the investor's resources obtains positioned in the chosen MIC without any in advance deal fees or trailer fees - Mortgage Investment Corporation. Amur Capital is concentrated on giving capitalists at any type of level with access to professionally took care of personal mutual fund. Investment in our fund offerings is readily available to Alberta, British Columbia, Manitoba, Nova Scotia, and Saskatchewan locals and must be made on a personal placement basis

Spending in MICs is a great method to acquire exposure to Canada's successful realty market without the demands of active home administration. Besides this, there are several various other reasons why capitalists take into consideration MICs in Canada: For those looking for returns comparable to the stock exchange without the linked volatility, MICs supply a secured actual estate investment that's less complex and may be more successful.

As a matter of fact, our MIC funds have actually traditionally delivered 6%-14% annual returns. * MIC capitalists receive rewards from the interest settlements made by customers to the home mortgage lender, creating a consistent passive revenue stream at higher prices than traditional fixed-income safeties like government bonds and GICs. They can likewise pick to reinvest the dividends into the fund for worsened returns.

Not known Facts About Mortgage Investment Corporation

MICs currently account for approximately 1% of the general Canadian home loan market and stand for an expanding sector of non-bank economic firms. As capitalist demand for MICs expands, it is necessary to understand how they work and what makes them different from traditional property investments. MICs buy mortgages, unreal estate, and for that reason offer exposure to the housing market without the included threat of residential or commercial property ownership or title transfer.

usually between 6 and 24 months) (Mortgage Investment Corporation). In return, the MIC accumulates like it passion and charges from the customers, which are then distributed to the fund's favored investors as returns repayments, usually on a regular monthly basis. Since MICs are not bound by most of the same rigorous borrowing demands as conventional banks, they can establish their very this content own criteria for approving lendings

This suggests they can bill higher interest prices on home loans than conventional financial institutions. Home loan Investment Firms likewise delight in unique tax treatment under the Earnings Tax Act as a "flow-through" financial investment lorry. To stay clear of paying earnings taxes, a MIC should distribute 100% of its take-home pay to investors. The fund should contend least 20 investors, without any investors having greater than 25% of the exceptional shares.

The 3-Minute Rule for Mortgage Investment Corporation

In the years where bond returns constantly decreased, Home mortgage Financial investment Corporations and other alternative properties grew in appeal. Returns have recoiled since 2021 as main financial institutions have increased rate of interest yet real yields continue to be negative about rising cost of living. Comparative, the CMI MIC Balanced Home loan Fund created an internet yearly yield of 8.57% in 2022, not unlike its efficiency in 2021 (8.39%) and 2020 (8.43%).

MICs offer financiers with a means to spend in the actual estate sector without in fact owning physical home. Instead, financiers pool their money with each other, and the MIC makes use of that cash to money home loans for debtors.

The Main Principles Of Mortgage Investment Corporation

That is why we wish to aid you make an informed choice regarding whether or not. There are numerous benefits linked with buying MICs, consisting of: Given that financiers' money is pooled together and spent throughout multiple residential properties, their portfolios are expanded throughout different property kinds and borrowers. By owning a portfolio of home mortgages, financiers can mitigate danger and avoid placing all their eggs in one basket.